Chargebacks and Disputes Your Rights as a Consumer

Understand the chargeback process and your rights when disputing fraudulent transactions. Learn how to protect your money and navigate financial disputes effectively.

Chargebacks and Disputes Your Rights as a Consumer

Understand the chargeback process and your rights when disputing fraudulent transactions. Learn how to protect your money and navigate financial disputes effectively.Ever made an online purchase only to find the item wasn't what you expected, or worse, never arrived? Or perhaps you've spotted a mysterious charge on your bank statement that you definitely didn't authorize. These situations can be incredibly frustrating and, frankly, a bit scary. But here's the good news: as a consumer, you have powerful tools at your disposal to fight back and reclaim your money. We're talking about chargebacks and disputes. These aren't just fancy financial terms; they're your rights, designed to protect you from fraud, errors, and unfulfilled promises.

In this comprehensive guide, we're going to break down everything you need to know about chargebacks and disputes. We'll cover what they are, how they work, when you should use them, and most importantly, how to successfully navigate the process. Whether you're in the US or Southeast Asia, understanding these mechanisms is crucial for safeguarding your financial well-being in an increasingly digital world. So, let's dive in and empower you with the knowledge to protect your hard-earned cash!

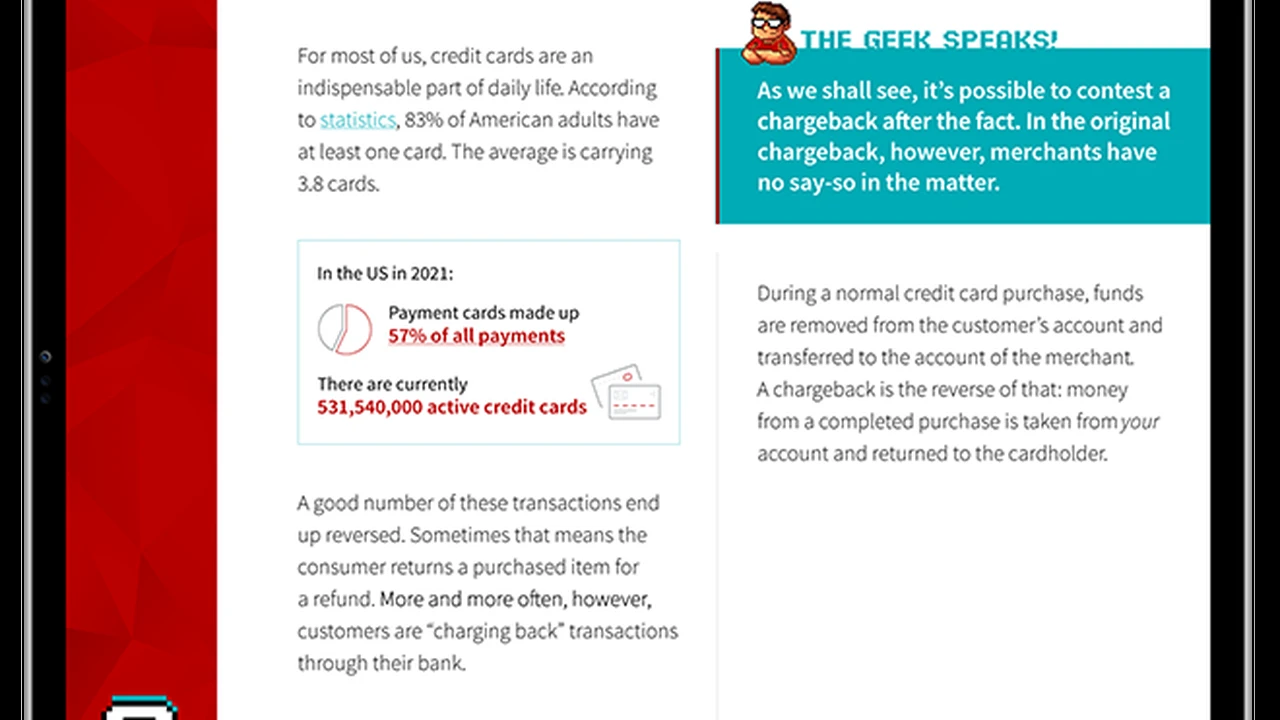

Understanding Chargebacks and Disputes What They Are

First things first, let's clarify what we're talking about. While often used interchangeably, 'dispute' is the broader term, encompassing any disagreement you have with a merchant or a transaction. A 'chargeback' is a specific type of dispute initiated by your bank or credit card issuer on your behalf, reversing a transaction and returning funds to your account. Think of it this way: all chargebacks are disputes, but not all disputes lead to a chargeback.

What is a Chargeback Consumer Protection Explained

A chargeback is essentially a forced refund. When you initiate a chargeback, you're asking your bank or credit card company to reverse a charge that you believe is illegitimate or incorrect. This isn't just a courtesy; it's a consumer protection mechanism built into the payment card networks (like Visa, Mastercard, American Express, and Discover). These networks have rules that protect cardholders from various issues, including:

- Fraudulent Transactions: This is probably the most common reason. If your card details are stolen and used without your permission, a chargeback is your primary recourse.

- Non-Receipt of Goods or Services: You paid for something, but it never arrived, or the service was never rendered.

- Goods or Services Not as Described: The item you received is significantly different from what was advertised or agreed upon. Think of ordering a brand-new smartphone and receiving a broken, used one.

- Duplicate Charges: You were charged twice for the same transaction.

- Incorrect Amount Charged: The merchant charged you more than the agreed-upon price.

- Credit Not Processed: You returned an item, and the merchant agreed to a refund, but it never appeared on your statement.

- Cancellation Issues: You canceled a subscription or service, but the merchant continued to charge you.

The beauty of a chargeback is that it shifts the burden of proof from you to the merchant. Once you initiate a chargeback, the merchant has to prove to the bank that the charge was legitimate and that they fulfilled their end of the bargain. If they can't, you get your money back.

Disputes Beyond Chargebacks Direct Merchant Resolution

Before jumping straight to a chargeback, it's often recommended to try resolving the issue directly with the merchant. This is what we call a 'dispute' in its broader sense. Many issues can be resolved quickly and amicably by contacting customer service. For example, if an item is slightly damaged, the merchant might offer a partial refund or a replacement without the need for bank intervention. This approach can be faster and less stressful for everyone involved. However, if the merchant is unresponsive, uncooperative, or outright refuses to resolve the issue, then a chargeback becomes your next, more powerful step.

When to Initiate a Chargeback Protecting Your Purchases

Knowing when to pull the trigger on a chargeback is key. It's a powerful tool, but it shouldn't be your first resort for every minor inconvenience. Here's a breakdown of scenarios where a chargeback is appropriate and often necessary:

Fraudulent Activity Unauthorized Transactions

This is the clearest case for a chargeback. If you see charges on your statement that you absolutely did not make, your card has likely been compromised. Act immediately! Contact your bank or credit card issuer, report the fraudulent activity, and request a chargeback. They will usually cancel your card and issue a new one to prevent further unauthorized use. This is where the Fair Credit Billing Act (FCBA) in the US, and similar consumer protection laws in Southeast Asia, really shine, limiting your liability for fraudulent charges.

Non-Delivery or Service Failure Unreceived Goods

You ordered a product online, paid for it, and it never showed up. Or you paid for a service (like a concert ticket or a subscription) that was never provided. After giving the merchant a reasonable chance to rectify the situation (e.g., by contacting their customer service), if you're still left empty-handed, a chargeback is warranted. Keep records of your attempts to contact the merchant.

Merchandise or Service Not as Described Significant Discrepancies

This can be a bit more nuanced. If you ordered a red shirt and received an orange one, that might be a minor discrepancy. But if you ordered a brand-new iPhone and received a brick, or a used, broken phone, that's a significant difference. The key is whether the item or service is materially different from what was advertised. If it renders the purchase unusable or significantly devalues it, then a chargeback is a valid option. Again, try to resolve it with the merchant first, and document everything (photos, emails, chat logs).

Billing Errors Duplicate Charges Incorrect Amounts

Sometimes, it's just a mistake. You might be charged twice for the same item, or the amount on your statement doesn't match the price you agreed to. While these can often be resolved directly with the merchant, if they're unwilling or unable to correct the error, a chargeback ensures you're only paying what you owe.

Unprocessed Credits or Refunds Merchant Refusal

You returned an item, the merchant confirmed the return and promised a refund, but weeks go by, and the money never appears. Or you canceled a recurring service, but the charges keep coming. If the merchant fails to process a promised credit or refund within a reasonable timeframe, a chargeback can force their hand.

The Chargeback Process Step by Step Guide

Navigating the chargeback process can seem daunting, but it's manageable if you know the steps. Here's a general outline, though specific details might vary slightly depending on your bank and card network:

Step 1 Contact the Merchant First Attempt Resolution

As mentioned, this is almost always the recommended first step. Gather all relevant information: order numbers, dates, descriptions of the issue, and any communication you've had with the merchant. Clearly explain the problem and what resolution you're seeking (e.g., a full refund, a replacement). Give them a reasonable amount of time to respond and resolve the issue (e.g., 7-14 business days). Document every interaction: save emails, take screenshots of chat logs, and note down dates, times, and names of customer service representatives if you call.

Step 2 Gather Your Evidence Documentation is Key

If the merchant is uncooperative or unresponsive, it's time to prepare for a chargeback. The more evidence you have, the stronger your case. This includes:

- Transaction details: date, amount, merchant name.

- Order confirmation emails or receipts.

- Screenshots of product descriptions or advertisements (especially if the item was not as described).

- Photos or videos of the received item (if damaged or incorrect).

- Shipping tracking information (if applicable).

- Records of your attempts to contact the merchant (emails, chat logs, call notes).

- Any terms and conditions related to returns or cancellations.

Step 3 Contact Your Bank or Card Issuer Initiate the Chargeback

This is where you formally initiate the chargeback. You can usually do this by calling the customer service number on the back of your card, logging into your online banking portal, or visiting a branch. Be prepared to provide:

- Your account information.

- The specific transaction details you want to dispute.

- A clear explanation of why you are disputing the charge (e.g., 'unauthorized transaction,' 'merchandise not received,' 'service not as described').

- All the evidence you've gathered.

Your bank will then open a formal dispute case. They will typically issue you a provisional credit for the disputed amount while they investigate. This means the money is temporarily returned to your account, but it's not final until the investigation concludes.

Step 4 The Investigation Process Merchant Response

Once your bank receives your dispute, they will contact the merchant's bank. The merchant's bank will then notify the merchant, who has a limited time (usually 30-45 days) to respond and provide their own evidence to refute your claim. This evidence might include proof of delivery, signed receipts, communication logs showing you agreed to the charge, or proof that the item was as described. If the merchant fails to respond or their evidence is insufficient, you win the chargeback, and the provisional credit becomes permanent.

Step 5 Resolution and Appeals Final Decision

If the merchant provides compelling evidence, your bank might reverse the provisional credit, meaning you'd have to pay the charge. However, you usually have the right to appeal this decision if you believe your evidence is stronger or the merchant's evidence is flawed. This might involve providing additional information or clarifying points. The entire process can take anywhere from a few weeks to several months, depending on the complexity of the case and the responsiveness of all parties involved.

Key Regulations and Timelines Consumer Rights US and SEA

Understanding the legal frameworks and timelines is crucial for a successful chargeback. While specific laws vary, the underlying principles of consumer protection are similar across regions.

United States Fair Credit Billing Act FCBA

In the US, the Fair Credit Billing Act (FCBA) is your best friend when it comes to credit card disputes. It applies to 'billing errors' on open-end credit accounts (like credit cards). Key protections include:

- Limited Liability for Fraud: For unauthorized credit card use, your liability is capped at $50, and often, card issuers waive this entirely if you report it promptly.

- Dispute Period: You generally have 60 days from the date your statement was mailed (or made available electronically) to dispute a billing error.

- Merchant Location: For disputes related to goods or services not delivered or not as described, the FCBA allows you to withhold payment for disputed amounts if the purchase was made in your home state or within 100 miles of your billing address, and the purchase amount was over $50. This specific clause is less frequently used now due to broader chargeback rules, but it's good to know.

For debit card transactions, the Electronic Fund Transfer Act (EFTA) provides similar, though slightly different, protections. Your liability for unauthorized debit card transactions can be higher if not reported quickly, so immediate action is vital.

Southeast Asia Consumer Protection Laws Regional Overview

Consumer protection laws in Southeast Asia are evolving, with many countries strengthening their frameworks. While there isn't a single overarching law like the FCBA for the entire region, individual countries have robust protections:

- Singapore: The Consumer Protection (Fair Trading) Act (CPFTA) protects consumers against unfair practices. While not directly a chargeback law, it provides avenues for redress, and banks generally follow international card network rules for chargebacks.

- Malaysia: The Consumer Protection Act 1999 (CPA) covers various aspects of consumer rights, including misleading conduct and defective goods. Financial institutions adhere to card network rules for chargebacks.

- Thailand: The Consumer Protection Act B.E. 2522 (1979) provides general consumer rights. The Bank of Thailand also has regulations concerning electronic transactions and dispute resolution.

- Philippines: The Consumer Act of the Philippines (Republic Act No. 7394) protects consumers against deceptive, unfair, and unconscionable sales acts and practices.

- Indonesia: The Consumer Protection Law (Law No. 8 of 1999) provides a framework for consumer rights and dispute resolution.

Across all these regions, the rules set by Visa, Mastercard, American Express, etc., largely govern the chargeback process. These networks have their own operating regulations that banks must follow, ensuring a relatively consistent process globally. Generally, you have a window of 120 days to 180 days from the transaction date (or the date you expected to receive goods/services) to initiate a chargeback, though this can vary by reason code and card network. Always check with your specific bank for their exact timelines.

Common Chargeback Scenarios and How to Handle Them Practical Advice

Let's look at some real-world examples and how you can best approach them.

Scenario 1 The Mysterious Charge Unrecognized Transactions

You check your bank statement and see a charge from 'XYZ Corp' for $75. You have no idea what XYZ Corp is or why you were charged. This is a classic case of an unrecognized transaction, which could be fraud or a legitimate charge you simply don't remember (e.g., a free trial that rolled into a paid subscription).

- Action: First, do a quick online search for 'XYZ Corp' to see if it's a legitimate company and if you might have interacted with them. Check your email for any receipts or subscription confirmations. If you still can't identify it, contact your bank immediately. Report it as an unauthorized transaction. They will likely initiate a chargeback and issue you a new card.

Scenario 2 The Item Never Arrived Non-Delivery

You ordered a new gadget from an online store, paid for it, and the tracking shows it was delivered, but you never received it. Or the tracking shows it's stuck in transit indefinitely.

- Action: Contact the merchant first. Provide your order number and explain the situation. Ask them to investigate with the shipping carrier. If they can't resolve it (e.g., they claim it was delivered, but you have proof it wasn't, or they refuse to reship/refund), then gather all your evidence (order confirmation, tracking info, communication with merchant) and initiate a chargeback with your bank for 'merchandise not received.'

Scenario 3 The Product is Faulty or Not as Advertised Defective Goods

You bought a high-end blender online, but when it arrived, it didn't work, or it was a completely different, cheaper model than what was advertised.

- Action: Take photos or videos of the faulty/incorrect product. Document the discrepancy with the original product description. Contact the merchant, explain the issue, and request a return/refund or replacement. If they refuse or offer an unsatisfactory solution, provide your bank with all your evidence (photos, product description, communication with merchant) and file a chargeback for 'merchandise not as described' or 'defective goods.'

Scenario 4 The Recurring Charge You Canceled Subscription Issues

You signed up for a free trial of a streaming service, canceled it before the trial ended, but you're still being charged monthly.

- Action: Check your cancellation confirmation (if you received one). Contact the merchant's customer service, provide proof of cancellation, and demand a refund for the erroneous charges. If they don't comply, gather your cancellation proof and bank statements showing the charges, then file a chargeback for 'credit not processed' or 'canceled service.'

Preventing Disputes and Fraud Best Practices for Consumers

While chargebacks are a great safety net, prevention is always better than cure. Here are some tips to minimize your chances of needing to dispute a transaction:

Secure Online Shopping Habits Vigilance is Key

- Shop on Reputable Sites: Stick to well-known, trusted retailers. If you're trying a new site, do a quick search for reviews.

- Look for HTTPS: Always ensure the website address starts with 'https://' and has a padlock icon in the browser bar. This indicates a secure connection.

- Read Reviews: Check product and seller reviews before making a purchase.

- Beware of Too Good to Be True Deals: Scammers often lure victims with unbelievably low prices.

- Use Strong Passwords: Especially for your online shopping accounts.

Monitoring Your Accounts Regular Statement Checks

Make it a habit to regularly review your bank and credit card statements. Don't wait for your monthly statement; many banks offer real-time transaction alerts via email or app notifications. The sooner you spot an unauthorized or incorrect charge, the easier it is to dispute it within the required timelines.

Using Secure Payment Methods Credit Cards vs Debit Cards

When shopping online, credit cards generally offer more protection than debit cards. As discussed, the FCBA provides strong protections for credit card users, limiting liability for fraud. While debit cards also have some protections under the EFTA, the process can be more complicated, and your liability might be higher if you don't report fraud immediately. When a debit card is compromised, the money is immediately taken from your checking account, which can cause issues with other bills or direct debits. With a credit card, you're disputing the bank's money, not your own, which is a significant advantage.

Virtual Credit Cards and One Time Use Numbers Enhanced Security

Some banks and third-party services offer virtual credit card numbers or one-time use card numbers. These are temporary card numbers linked to your actual credit card but can only be used for a single transaction or for a limited time/merchant. If a virtual number is compromised, your actual card details remain safe. This is an excellent layer of protection for online purchases, especially from less familiar merchants.

Keeping Records of Purchases and Communications Digital Paper Trail

Always save order confirmations, shipping notifications, and any communication you have with merchants. This digital paper trail is invaluable if you ever need to dispute a charge. Create a dedicated folder in your email for online purchase receipts.

Beyond Chargebacks Other Consumer Recourse Options

While chargebacks are powerful, they aren't the only avenue for consumer protection. Sometimes, other options might be more suitable or can be pursued in conjunction with a dispute.

Consumer Protection Agencies Government Oversight

In both the US and Southeast Asia, government agencies are dedicated to protecting consumer rights. These agencies can often mediate disputes or take action against businesses engaging in unfair practices.

- United States: The Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB) are key agencies. You can file complaints with them, and while they don't directly resolve individual disputes, they use complaints to identify patterns of fraud and take enforcement actions against companies. State Attorney Generals also have consumer protection divisions.

- Southeast Asia: Each country has its own consumer protection bodies. For example, the National Consumer Affairs Council (NCAC) in the Philippines, the Ministry of Domestic Trade and Consumer Affairs (KPDNHEP) in Malaysia, and the Consumers Association of Singapore (CASE). These bodies can offer advice, mediation services, and sometimes even legal assistance.

Online Dispute Resolution Platforms Third Party Mediation

For e-commerce transactions, some platforms offer their own dispute resolution services. For example, PayPal has a robust Buyer Protection program that allows you to dispute transactions made through their platform. Similarly, marketplaces like Amazon or eBay have their own resolution processes for purchases made through their sites. These can often be faster than a bank chargeback, especially for issues like non-receipt or items not as described.

Small Claims Court Legal Recourse

For larger disputes where other avenues have failed, small claims court can be an option. This is typically for disputes involving amounts below a certain threshold (which varies by jurisdiction) and doesn't usually require a lawyer, making it more accessible. However, it can be time-consuming and should generally be considered a last resort.

Navigating the Digital Landscape Empowering Your Financial Security

In an increasingly digital world, where transactions happen at the speed of light and across borders, understanding your rights as a consumer is more important than ever. Chargebacks and disputes are not just technical processes; they are fundamental safeguards that empower you to shop, bank, and transact online with greater confidence. By being vigilant, documenting your purchases, and knowing when and how to exercise your rights, you become your own best advocate against fraud and unfair practices. So, go forth, shop smart, and remember: your money, your rights!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)